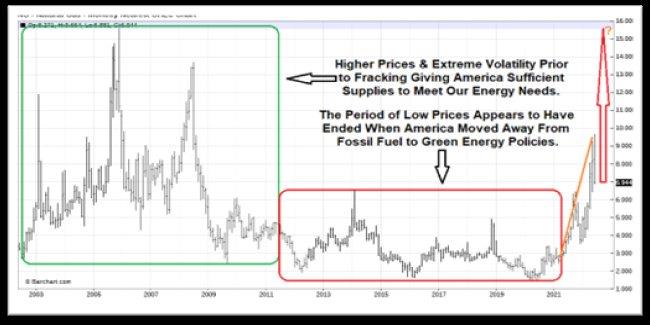

In my May 31st Energy Update, I discussed three risk factors increasing the risk Natural Gas could be higher this summer. The first factor was the EIA’s May 10th Short Term Energy Outlook (STEO) forecasting supplies would start the summer cooling period 14% below the 5-year average and Natural Gas would respond by averaging $8.59/MMBtu in the second half of 2022.

But the delay in reopening Freeport LNG, which accounts for about 20% of U.S. LNG exports decreases exports of LNG overseas by nearly 2 Bcf/d allowing more supplies to remain in storage in the U.S. for the generation of electricity. While this will likely decrease the supply deficit to the 5-year average, it is not expected to totally eliminate it.

Goldman Sachs Commodities Research following the latest Freeport outage news revised its end-October storage estimate to just over 3,500 Bcf, versus 3,424 Bcf predicted in April. “This remains a low storage level relative to history,” Goldman analysts Samantha Dart, Damien Courvalin, and Romain Langlois said in a research note, and should our U.S. Natural Gas balances be tighter than expected in the coming months, the risk remains that U.S. Natural Gas prices may need to trigger max substitution towards Appalachia coal, which we estimate would require a sustained gas price rally to around $12/MMBtu.”

The question is even with the delay in reopening Freeport LNG, what would cause supplies to be tighter than expected this summer?

The answers are found in the second and third risk factors discussed in the May 31st Energy Update. NOAA’s forecast of a warmer than normal summer increasing Natural Gas demand and NOAA’s forecast of an active hurricane season with very intense storms possible due to loop current in the Gulf leading to hurricanes similar to Katrina in 2005, resulting in supply disruptions and higher Natural Gas prices.

Therefore, although the delay in reopening Freeport LNG does lessen the risk of higher Natural Gas prices this summer, the risk for higher prices is still higher than normal, and longer-term the delay in reopening could increase the risk of higher Natural Gas prices long-term.

But the delay in reopening Freeport LNG, which accounts for about 20% of U.S. LNG exports decreases exports of LNG overseas by nearly 2 Bcf/d allowing more supplies to remain in storage in the U.S. for the generation of electricity. While this will likely decrease the supply deficit to the 5-year average, it is not expected to totally eliminate it.

Goldman Sachs Commodities Research following the latest Freeport outage news revised its end-October storage estimate to just over 3,500 Bcf, versus 3,424 Bcf predicted in April. “This remains a low storage level relative to history,” Goldman analysts Samantha Dart, Damien Courvalin, and Romain Langlois said in a research note, and should our U.S. Natural Gas balances be tighter than expected in the coming months, the risk remains that U.S. Natural Gas prices may need to trigger max substitution towards Appalachia coal, which we estimate would require a sustained gas price rally to around $12/MMBtu.”

The question is even with the delay in reopening Freeport LNG, what would cause supplies to be tighter than expected this summer?

The answers are found in the second and third risk factors discussed in the May 31st Energy Update. NOAA’s forecast of a warmer than normal summer increasing Natural Gas demand and NOAA’s forecast of an active hurricane season with very intense storms possible due to loop current in the Gulf leading to hurricanes similar to Katrina in 2005, resulting in supply disruptions and higher Natural Gas prices.

Therefore, although the delay in reopening Freeport LNG does lessen the risk of higher Natural Gas prices this summer, the risk for higher prices is still higher than normal, and longer-term the delay in reopening could increase the risk of higher Natural Gas prices long-term.