Energy News: Mild Weather Decreases Natural Gas Demand and Prices Plunge to Near All-time Low

Energy News Report: February 19th, 2024 Mild Weather Decreases Natural Gas Demand and Prices Plunge to Near All-time Low https://youtu.be/09oiFHLZgds

Energy News Report: February 19th, 2024 Mild Weather Decreases Natural Gas Demand and Prices Plunge to Near All-time Low https://youtu.be/09oiFHLZgds

Energy News Report: February 19th, 2024

In our February 5th Energy Update we recommended taking advantage of the short-term decline caused by the January thaw in conjunction with Freeport LNG temporarily closing one of their liquefaction units, and reserve energy to be available when present agreements expire.

But after writing our February 5th Energy Update, all major weather models unexpectedly extended their forecast of milder than normal weather through the end of February, which is expected to increase the already higher than normal total supplies on February 5th by more than 100 Bcf by March 8th. Total Natural Gas supplies are now projected to be approximately 2,260 Bcf by March 8th, which would be 34% above the 5-year moving average.

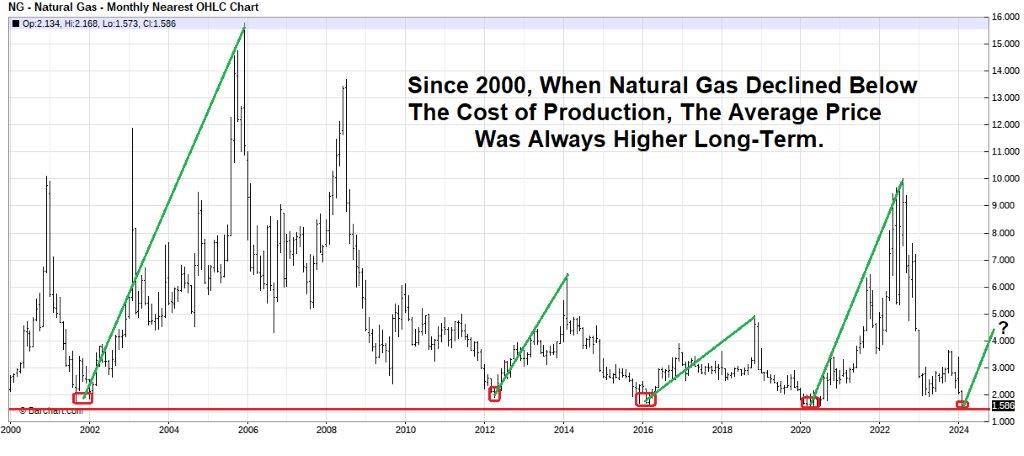

The unexpected increase of supplies in storage pushed prices below long-term support near $2 per MMBtu:

Prices breaking below long-term support near $2.00 per MMBtu due to total supplies projected to be 2,260 Bcf by March 8th was unexpected, the question is, based on what has happened in the past will prices remain near today’s very low prices for an extended period or are they expected to move higher this year?

We will answer this question by presenting you with historical data, and trust the data will guide your decision-making.

To do so, our goal was to research whether there were historical instances in which supplies were as high as today and analyze Natural Gas’s response long term to those high supply levels.

We reviewed data from the Energy Information Administration’s website, and discovered in 2012 and 2016, the total supplies of Natural Gas were higher than where they are estimated to be this year on March 8th. The dates were based on weekly historical data taken from the previous Friday’s close, and those dates didn’t fall precisely on March 8th, but were close to that date.

As pointed out earlier, our total supplies are projected to be approximately 2,260 Bcf by March 8th, but as you can see in the above charts, on Mar 9th, 2012, we had 2,369 Bcf in storage, and on Mar 11th, 2016, we had 2,478 Bcf in storage, and in both cases, Natural Gas prices were much higher by the end of the year.

In 2012, milder-than-normal weather continued until the end of March and prices declined into the middle of April before reaching their final low at $1.91 per MMBtu.

In 2016, the final low at $1.61 per MMBtu was reached in early March, and in both cases, Natural Gas more than doubled approaching $4.00 per MMBtu by the end of the year.

The question is, after reaching lows close to this time of year with total supplies higher than where they are today, why did prices more than double by the end of the year?

In both 2012 and 2016, similar to this year, we experienced warmer than normal winters resulting in supplies reaching record levels, but prices continued higher into the end of the year simply because prices were unsustainably low.

Prices are unsustainably low when they drop below the cost of production. It should also be noted that the longer prices stay low the higher they will go! This is a byproduct of the weaker companies being forced out of business thereby decreasing competition, and the surviving companies are highly motivated to increase prices to make up for lost profits accrued while prices were low.

The takeaway from this analysis is as we approach the lowest price since 2000, the conditions supporting a major bottom in Natural Gas are in place, and although prices could go slightly lower in the near term, the average price of Natural Gas will likely be significantly higher by the end of the year.

Therefore, if your present energy agreements expire in 2024 or 2025, we recommend you take advantage of this latest short-term decline caused by this year’s warmer-than-normal winter in conjunction with Freeport LNG temporarily closing one of their liquefaction units, and reserve energy to be available when your present agreements expire.

We believe the average price will be higher long-term, and the upside risk is far greater than the downside reward potential of waiting and hoping for slightly lower prices.

Not every client’s risk tolerance and hedging strategy are the same, but hopefully, today’s report will help put into perspective your risk/reward opportunities. We invite you to call one of our energy analysts to help you plan a hedging strategy appropriate for your situation.

Ray Franklin

Energy Professionals

Senior Commodity Analyst

Don't have one? You can get one by calling us at 855-4-PKIOSK.

Energy Professionals is committed to finding its customers the best possible rates on electricity and natural gas. Tell us your location and service type and our energy manager will connect you to the most competitive offers.

Switching to an alternate supplier is easy. There is no chance of service disruption, and you'll continue with your current utility for energy delivery and emergency service. Take a few minutes to discover your best offers, and enjoy the benefits of retail energy in your home or business.

1. Energy Type

2. Service Type

3. Zip Code

4.Local Company

5.Zone

We believe that knowledge is power. Here’s a free e-book that provides business solutions to reducing energy costs.

Download E-Book Free Energy Audit