Energy Update | May 29th, 2019

Energy Update May 29th, 2019 Natural Gas Spring Shoulder Ending and Risk of Higher Prices Increase as Prices Remain

Energy Update May 29th, 2019 Natural Gas Spring Shoulder Ending and Risk of Higher Prices Increase as Prices Remain

Energy Update

May 29th, 2019

In my Apr 22nd Energy Update, I explained why I believe prices must go higher longer-term, and the longer prices remain near today’s very low levels the higher they will go in the future.

My analysis was based on 4 Fundamental Facts:

1. The production of Natural Gas requires a large amount of ongoing capital investment (CAPEX). New wells must constantly be drilled to replace the huge volumes lost due to well depletions. When Natural Gas prices are high Exploration & Production companies have sufficient cash for the capital investment needed to drill new wells, but when prices are low, capital investment for new wells decline.

2. Demand for Natural Gas is expected to continue increasing due to exports of Liquified Natural Gas overseas, increased pipelines to Mexico and switching from Coal to Natural Gas for electric power generation.

3. Low Natural Gas prices has led to the ominous combination of E&P companies decreasing CAPEX resulting in less production, while increasing demand for exports and power for electric power generation. This combination is forcing many E&P companies to turn to debt for the capital needed to maintain production.

4. Low prices are a threat to many E&P companies’ long-term survival, which is demonstrated by the fact that over the last 3 years more than 100 Oil and Gas and companies have declared bankruptcy from January 2015 through December 2018, and Oil and Gas bankruptcies are accelerating.

In My Apr 18th Energy Update, I said the demand for Gas and Electricity always decline in the spring and fall prior to increasing again during the summer cooling and winter heating seasons, and over the years I have observed prices near cyclical and historical lows during “Shoulder Periods” are excellent buying opportunities and although prices could decline marginally from present levels, the upside risk was too great to justify waiting for slightly lower prices.

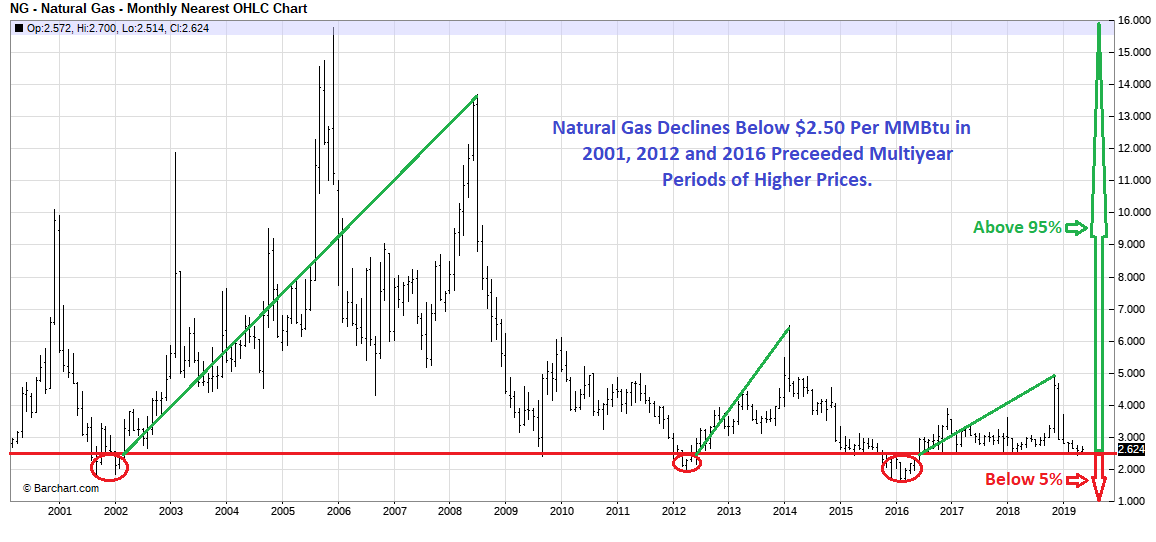

In today’s report, I update what Natural Prices have done since declining to long-term support during the spring “Shoulder Period”, and why the risk of higher prices is increasing as the spring ‘Shoulder Period” draws to a close. As you can see in the chart below, after writing my Apr 18th Energy Update, prices did fall marginally below long-term support near $2.50 per MMBtu for a few days prior to rebounding and remaining above long-term support.

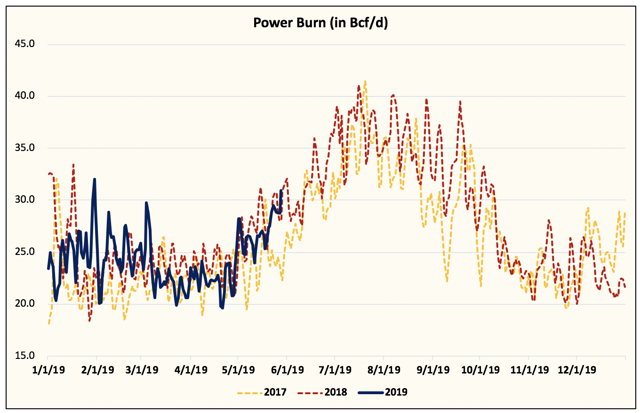

As the “Shoulder Period” draws to a close the demand for power to cool homes during the summer months will significantly increase the usage of Natural Gas and Electricity.

Increased demand for Natural Gas during the summer must be counterbalanced by corresponding growth in production. If production does not keep up with demand the result will be structural imbalances and higher prices. I am concerned production growth appears to be slowing, which could be the result of the 4 fundamental facts discussed earlier in this analysis. Low prices inhibit production growth and as I discussed in my Apr 22nd Energy Update, the longer prices stay low, the higher they will go later.

The one near-term unknown variable is the effect weather will have on demand this summer. A mild summer would decrease demand and prices could fall below $2.50 as we enter this year’s fall “Shoulder Period”. But as shown in last month’s report since 2000, there were 3 periods when Natural Gas was below $2.50 per MMBtu for a few months, and as you can see in the chart below, Natural Gas prices below $2.50 per MMBtu always preceded much higher prices for an extended period of time.

Conclusions:

Natural Gas has held above long-term support during this year’s spring “Shoulder Period” and since demand for power to cool homes during the summer months significantly increases, the risk of higher prices will also increase. The one near-term unknown is the effect weather will have on demand this summer. Although over the last 20 years prices have been higher than $2.50 per MMBtu 95% of the time, a mild summer would decrease demand and prices could fall below $2.50 as we enter this year’s fall “Shoulder Period”. But Natural Gas prices below $2.50 per MMBtu always preceded much higher prices long-term.

Therefore, I recommend anyone with agreements expiring within the next 18-months not delay hoping for lower prices, and reserve energy at today’s very low prices to be available when their present agreements expire. The upside risk is too great to justify waiting for slightly lower prices.

Not every client’s risk tolerance and hedging strategy is the same, but the above report will help you put into perspective the risk/reward opportunities. I invite you to call one of our energy analysts to help you plan a hedging strategy appropriate for your situation.

Ray Franklin

Energy Professionals

Senior Commodity Analyst

Energy Professionals is committed to finding its customers the best possible rates on electricity and natural gas. Tell us your location and service type and our energy manager will connect you to the most competitive offers.

Switching to an alternate supplier is easy. There is no chance of service disruption, and you'll continue with your current utility for energy delivery and emergency service. Take a few minutes to discover your best offers, and enjoy the benefits of retail energy in your home or business.

1. Energy Type

2. Service Type

3. Zip Code

We believe that knowledge is power. Here’s a free e-book that provides business solutions to reducing energy costs.

Download E-Book Free Energy Audit